since the 1980s, and increasingly, nominal and real growth have become more tightly knit.

A few weeks ago, following some back and forth with Unlearning Economics On the Lousy Reasoning Behind NGDP Targeting I commented:

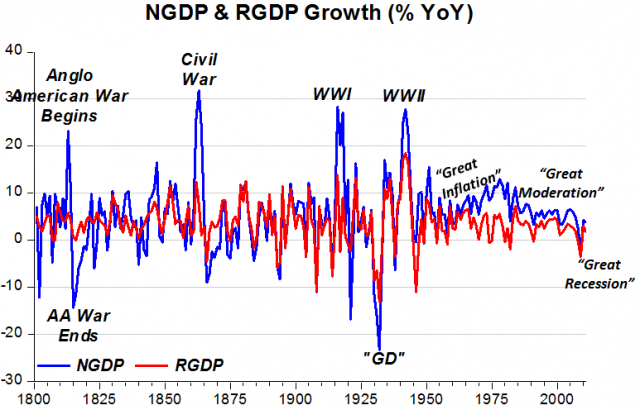

Woj - As long as the CB is reasonably successful at targeting low inflation, NGDP and RGDP will obviously be highly correlated over time. However, if the CB were to target quantity rather than price, I’d imagine that RGDP and NGDP might be less correlated. Is it possible that much of the correlation stems from current CB policy and that changing policy would also change the relationship?Attempting to support this view, I expanded on the topic in a couple posts: NGDP Targeting: Changing Policy Changes Relationships and NGDP Targeting: Changing Policy Changes Relationships (Part 2).

Yesterday I posed the following question to Marcus:

Why will changing policy to promote higher inflation today not cause a breakdown in the correlation of the past 30 years, similar to the 1970’s?Marcus was kind enough to not only reply, but also to direct me through email to his take on NGDP Targeting in The crisis from an AD perspective. The post is well constructed and a generally good read on the subject. The specific quote that struck comes near the end:

I wonder in what kind of world we would be living today if 20 years ago the group that argued for the stabilization of AD growth (level targeting) as the rule to be followed by MP had won the debate over those that proposed IT with the interest rate as the policy “instrument”. Quite likely we would be experiencing much less “fiscal stimulus” with all its attendant risks.Although I remain a skeptic on NGDP Targeting and the impact of monetary policy more broadly, I entirely agree that fiscal policy holds far more “attendant risks.” In choosing between flawed monetary policies, the one that reduces the need for “fiscal stimulus” may very well be favorable.

As I noted in a reply to Marcus and Saturos, my hesitation on NGDP Targeting stems from a Minsky/MMR view under which private credit creation/lending (through banks) can and currently does significantly influence aggregate demand. The ability of monetary policy to control NGDP would therefore be weak and skewed towards reducing NGDP. Further, the amount of monetary stimulus necessary to try and meet targets may not be politically feasible.

All that being said, I’m not exactly a supporter of inflation targeting either, as discussed in Inflation Targeting Shifted Fed Focus to Constraining Aggregate Demand. Hopefully, in time, the lessons from NGDP supporters and the Minsky/MMR crowd can align to find common ground on monetary policy. Until then I remain open to and interested in new methods of monetary policy (including free banking) that offer improvements over inflation targeting.

No comments:

Post a Comment