And so it is in the Eurozone: Spanish banks need recapitalization because of the deflationary policies forced on them to reduce Spain’s public sector deficit at a time when the private sector is also de-leveraging. Clearly this has a lot further to go and house prices will fall even further as a result. But the lesson from Japan was that overly focusing on the banks as ‘the problem’ is misguided and until or unless deeply deflationary policies are altered, the Spanish banks will be back for another bailout before too long.

This fits well with the case I previously laid out that private debt continues to drag down Europe.

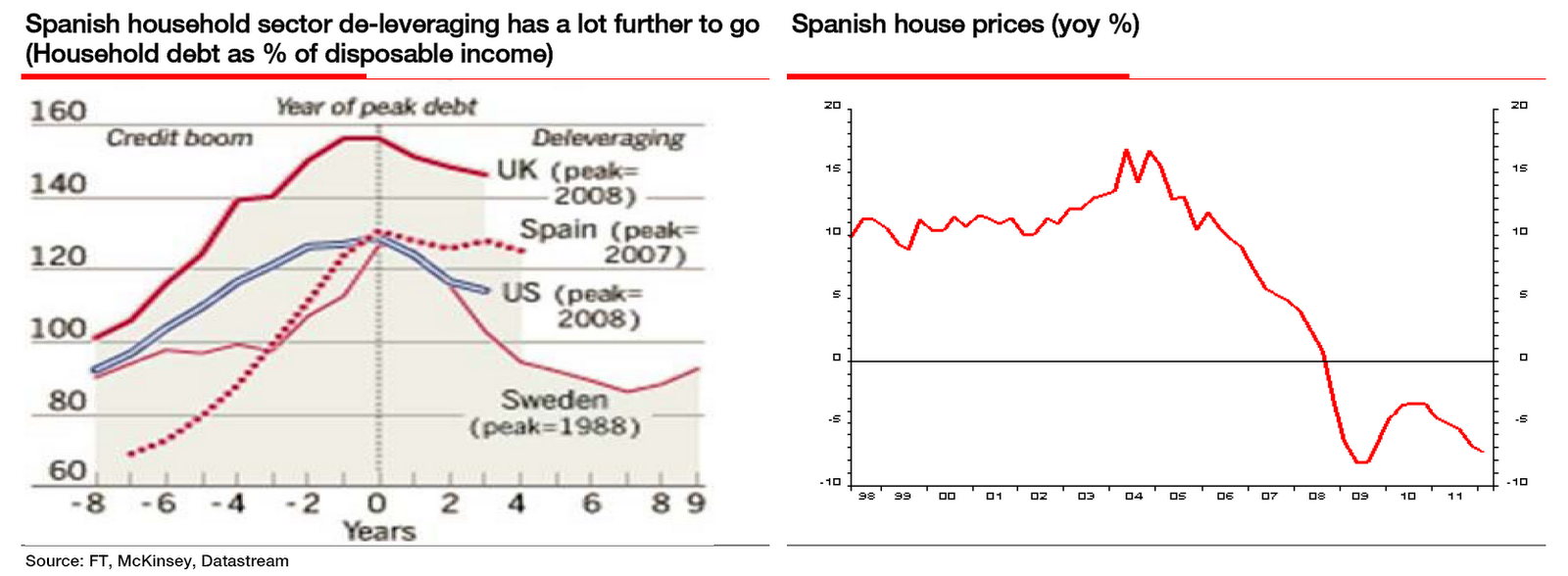

This above dynamic is especially important for understanding Spain, where sovereign debt levels (at least those officially reported) are not particularly high. Spain’s housing bubble, however, continues to decline putting further pressure on private sector balance sheets. The public and private sectors cannot both successfully deleverage, in tandem, without destroying incomes and growth.As the first chart from Edwards’ shows, households have not yet begun to seriously deleverage and unemployment is already well over 20%. This process will continue to put downward pressure on house prices, which may fall by another 35%. As prices fall Spanish banks will ultimately be forced to write down mortgage values, further impairing their balance sheets. By focusing the bailout on banks, Spain in not only following the path of Japan but also that of Ireland. Despite significantly larger bailouts relative to the size (GDP) of Ireland, Irish banks remain insolvent. Putting these pieces together, it becomes obvious that Spanish banks will require further bailouts.

A lesson pointed out in the title of Edward’s note that should have been learned from Japan is that “banks are not the problem.” Unfortunately Spain, Ireland and several other countries have made this same mistake during the current crisis. Private debt deleveraging, especially by households, is at the heart of the current crisis and remains unaddressed. Until private sector balance sheets return to health, economic growth will continue to languish (at best) and highly leveraged banks will become increasingly insolvent. For countries without the ability to print currency (ie. the Eurozone), use of public funds to bailout the banks may eventually topple the sovereigns.

Heading into another Euro Summit, I fail to see any signs that policy makers will soon change course and address private balance sheets. The crisis is speeding up but the policy solutions remain unsuitable for the problem at hand.

No comments:

Post a Comment